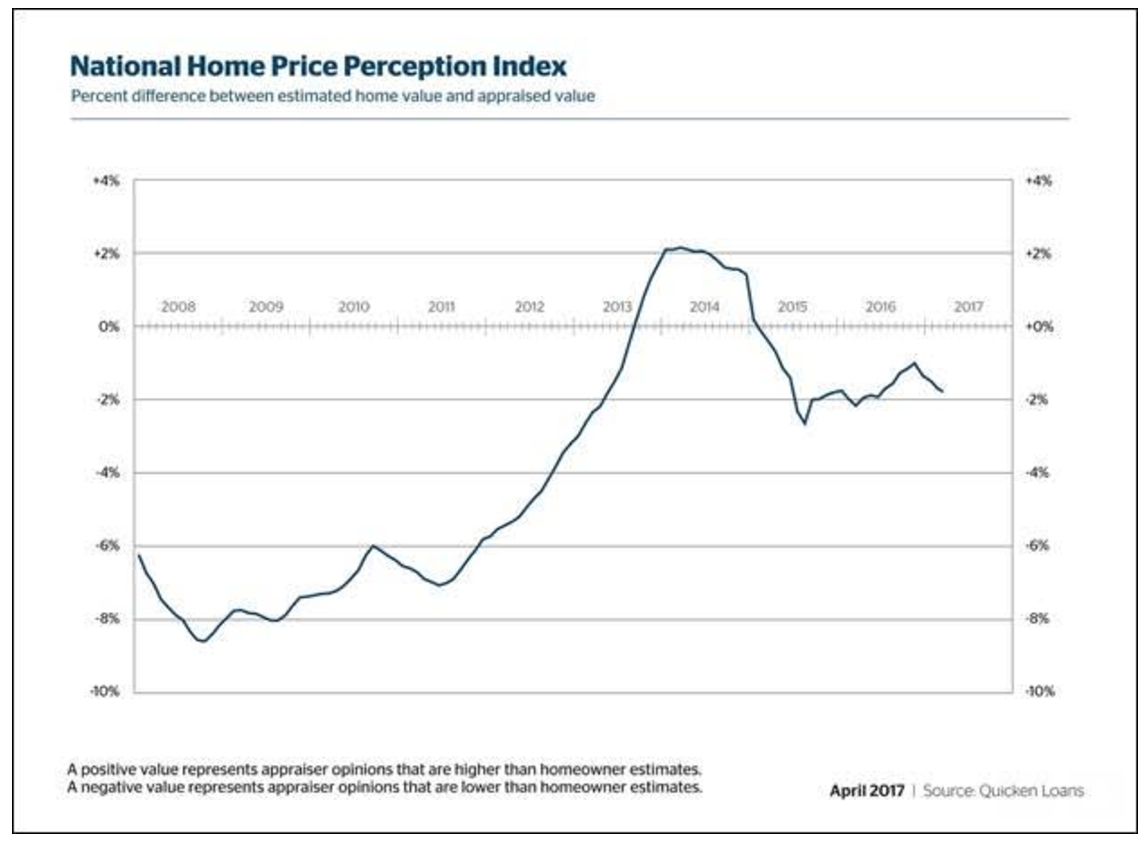

Home values continued their upward climb, however not quite as fast as homeowners estimated, according to Quicken Loans’ Home Price Perception Index.

On average, appraised home prices came in 1.77% lower than what homeowners expected, the fourth consecutive month the gap between the two opinions widened, according to the index.

Home values increased in March by 0.63% from February, but increased 3.3% from last year, the index shows.

This chart shows the difference between appraised home values and homeowner estimates over the past several years since 2008.

Click to Enlarge

(Source: Quicken Loans)

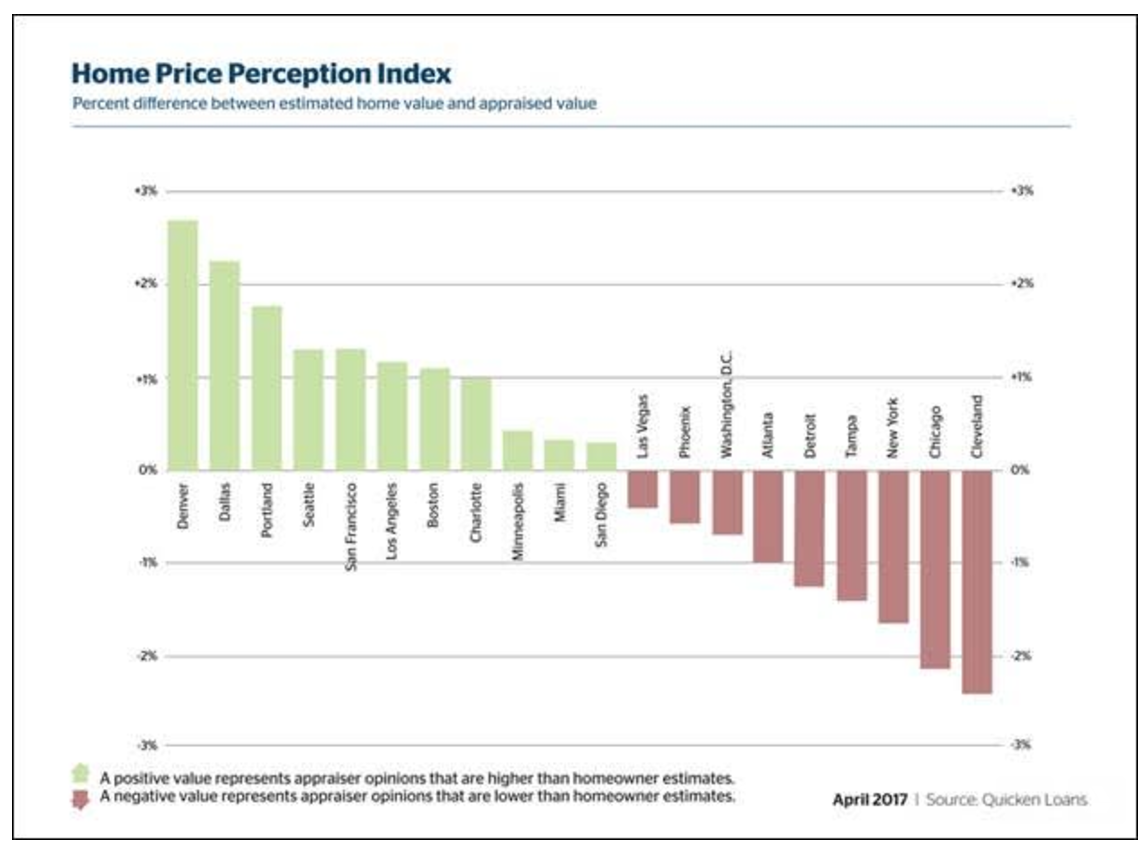

Home value perception varies across different areas of the country. In some markets, such as those on the West Coast, home prices are increasing so fast that homeowners can’t keep up as appraised values come in higher than their estimates.

“The national average shows appraisals lower than homeowner expectations, but some cities are bucking that trend,” said Bill Banfield, Quicken Loans vice president of capital markets. “With prices sprinting forward in many of the booming housing markets in the West, it can be difficult for homeowners to keep up with appraisers, who are on the ground, examining real estate price changes every day.”

“This study is one more reminder for consumers to keep an eye on their local market before selling or refinancing,” Banfield said. “The state of their local market could affect their home’s value – on either end of the spectrum.”

This chart shows a breakdown of markets across the U.S., and how homeowner estimates compare across the housing markets.

Click to Enlarge

(Source: Quicken Loans)